Al Lim discusses issues affecting Myanmar’s COVID-19 stimulus package and ways to improve it.

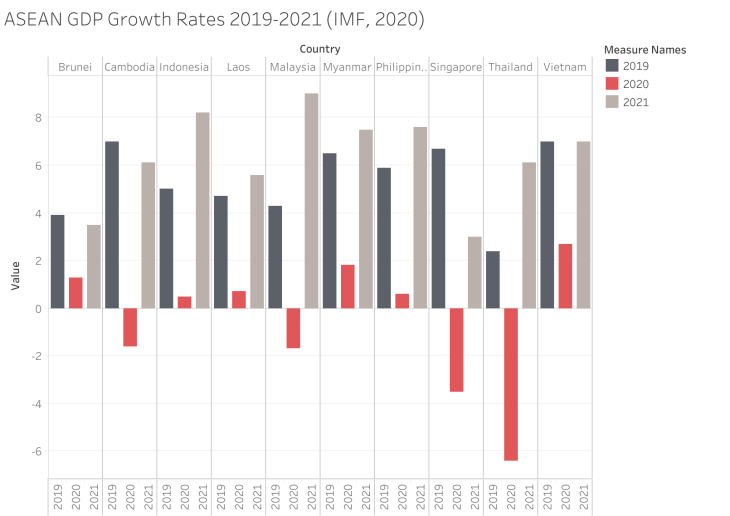

The economic shocks of COVID-19 have wreaked havoc across the world, and Myanmar is no exception. The country’s opening to international trade in 2011 and its connections with the global economy have made it vulnerable to global value chain disruption and distorted capital flows. Domestic shocks that accompany public health policies, such as lockdowns, have worsened the pandemic’s effects. The economic outlook is bleak: the International Monetary Fund (IMF) has projected that ASEAN’s growth of 4.3% in 2019 will be reduced to 1.2% in 2020. Myanmar’s forecast has also dropped from 6.5% (2019) to 1.8% (2020). This parallels the projected drop in most ASEAN economies for 2020 (Figure 1). Beyond GDP figures, the informal sector has been challenging to monitor but will be significantly affected in the short- and long-term.

This article contextualizes the macroeconomic fallout in Myanmar and identifies how its response—the COVID-19 Economic Relief Plan (CERP)—can be improved. Factors such as border restrictions and the sharp decline in tourism have consequences for many Burmese on the ground. These effects intersect with existing vulnerabilities and have resulted in employers and employees struggling to maintain their livelihoods, worsening the precarity of many populations.

To address these issues, the state issued the CERP to improve the situation. While there are some benefits from the plan such as supplying food or decreasing bank interest rates, it can be enhanced. This article suggests three improvements to the CERP: (1) the plan needs to clarify its financing, (2) re-evaluate its implementation through better communication between the different parts of the government (i.e. union, subnational, and township) and create more robust monitoring mechanisms, and (3) integrate social and environmental components with consultation and green stimulus measures. In doing so, the current plan can better address the existing and widening forms of precarity and vulnerability towards a more sustainable recovery.

The COVID-19 pandemic has generated unprecedented global value chain disruption, capital outflow from the Global South, and massive strains on the informal economy. The worldwide goods trade is touted to shrink 10-30% this year, due to restricted cargo transport, port closures, border restrictions, and limited internal movements. Myanmar is especially affected by the macroeconomic trends, having the lowest GDP per capita (gross) in Southeast Asia and 24.8% of the population under the poverty line,

These shocks have devastated Myanmar’s garment industry, which comprised more than 25% of its exports (US$3.79 billion) in 2017. The industry’s supply shock was precipitated by China cutting off the export of raw materials from January to March. China previously accounted for 90% of the raw materials needed in Myanmar’s garment industry. Subsequently, when China’s raw materials became available for export, international demand had collapsed. This has affected Myanmar’s 700,000 garment workers, half of whose jobs are threatened, with 25,000 laid off since mid-April. International efforts such as the “Myan Ku” package by the EU provide some economic relief but is inadequate compared to the industry’s scale.

In terms of international capital flows, while trade with ASEAN was healthy in the first half of Fiscal Year (FY) 19/20, global remittance flows are projected to decline by 20% in 2020 and there has been massive capital flight to safer currency havens. There are more than 3 million Burmese working overseas in Thailand and beyond, which contribute to a US$3.5 billion-dollar remittance flow, that has also been compromised due to the pandemic. Many have lost their jobs in their country of work and are forced to return home. Over 100,000 migrants have returned to Myanmar between March and June, mostly from Thailand, and many are experiencing worsened job prospects back home. Return migrants also face social stigma due to the nature of COVID-19’s imported cases to Myanmar, compounding the severity of their situation.

Additionally, the aviation and tourism industries have drastically fallen with global travel restrictions. According to the World Travel and Tourism Council (WTTC), travel and tourism in Myanmar employs over a million workers (4.8% employment) and contributes 4.6% to the total GDP. An impact analysis by the International Air Transport Association (IATA) has Burmese passenger demand in aviation reduced by 48% between 2019 and 2020, with a revenue impact of over US$690 million. Many hotels and tour operators have shuttered since the border restrictions and lockdowns, reducing the 4 million travelers in 2019 to a trickle in 2020.

One of the biggest, and hardest to quantify, parts of the Burmese economy is its informal sector, which comprises home-based employment, subcontracted jobs, or family businesses not registered with the state. This sector employs over 18 million workers (83% of Myanmar’s labor force), and has been disproportionately impacted by the public health responses to the pandemic. For instance, the construction industry employs many informal workers, and sites have been limited to 50 workers according to the Ministry of Health and Sports since April even though some sites usually have more than 1,000 workers. These construction companies thus face a double-bind: they have to choose to retain or fire their employees while dealing with the possible suspension of projects and the loans they had taken to finance the projects. More generally, workers in the informal sector lack basic job protections and access to social security schemes.

How do these indicators and economic impacts play out on the ground? The economic effects of the pandemic intersect with existing vulnerabilities of the Burmese population. Here, I include two vignettes that illustrate how a cross-border supply chain disruption and tourist-dependent industry have been affected, showing the material consequences of the macroeconomic effects on the ground. It contextualizes these macroeconomic trends, showing how they intersect with pre-existing issues such as pollution and the current pandemic.

First, fruit businesses are experiencing the brunt of global value chain disruptions, suffering from significant revenue losses due to China-Myanmar border restrictions (Figure 2). China only allows 300 trucks to cross the border, resulting in massive pile-ups, and has closed 11 checkpoints for several months (other than for trade). So, the Burmese drivers hand their trucks over to their Chinese counterparts at the border, which in itself is a logistical nightmare. Companies are reporting that they are unable to even cover transport costs, losing 3-4 million kyat (US$2,000-3,000).

This vignette illustrates how COVID-19 policies have resulted in supply chain disruption, and their effects on the ground. The global supply chain built on short-term revenue gain created the pre-COVID current networks of distribution. Since the coronavirus pandemic, border restrictions and heightened demand-side risk due to the fiscal dependence on exports has exacerbated susceptibility to undernutrition and deficiencies. It is ironic that large swathes of Myanmar are malnourished and experiencing hunger, yet rotten fruits pile at its border. The World Food Programme’s (WFP) hunger map reports that 15.2 million people have insufficient food and 29.4% of children under 5 are reporting chronic malnutrition at the time of writing.

These are urgent issues with visceral consequences, and the WFP’s map reveals a differentiated geography of inter-state hunger. For example, Yangon has 25% of its population with insufficient food consumption, compared to Chin state with 64% and Shan state with over 40%. This highlights broader the inter-state poverty trends stated in a World Bank report on the country’s poverty, where Chin state has a poverty rate of 71% and Shan in the mid-40s. Therefore, the multi-dimensional effects of poverty such as malnutrition manifest through existing inter-state inequalities, widening socioeconomic gaps in the country.

Border trade disruptions raise important questions for post-COVID Myanmar—are there shorter, more resilient food supply chains that can mitigate these issues? Is there a way that a more circular economic model can be used to disaster-proof the fruit trade? This is especially vital given international global trends of regionalization and deglobalization.

Besides issues of exports and international trade, and domestic industries such as tourism have taken severe hits. At Inle Lake, residents’ livelihoods are at risk. They are complaining that water levels have dropped. While the water level’s change can be attributed to environmental variability, its drop exacerbates a host of COVID-19 generated issues.

Residents cannot travel around the lake, irrigate their fields, or gain revenue from tourists. Further, the lake’s reduced water level has been an accumulation of externalities from hotel construction, chemical fertilizers, and climate change. The long-term build-up of effects coupled with the short-term issues brought about by the pandemic has culminated in large impacts for these workers and their livelihoods. Many around the country are also in the tourism and agriculture sectors, making up sizeable parts of Myanmar’s GDP. Lower sales and the price of produce severely affect farmers, who are also unable to access adequate financing options for the coming planting season. Tourism businesses are struggling to stay afloat, and have emphasized the inadequacy of the government’s efforts to support them.

The pandemic’s impacts extend long beyond short-term disruptions: farmers unable to plant, pay back their debts, and gain new revenue; and many tourism businesses permanently shuttering. Understanding that the pandemic has generated new problems for many local businesses and industries, it is necessary for a whatever-it-takes response to ensure lives and livelihoods are protected.

The plan’s financing remains quite unclear. The CERP is estimated to cost US$2-3 billion, subjected to pending loans according to the Ministry of Planning, Finance and Industry (MOPFI). It would probably be financed through some national budget reallocation, the IMF’s Rapid Credit Facility (RCF) and Rapid Financing Instrument (RFI), as well as with the World Bank and Asian Development Bank’s support. While the Parliament has approved a US$700 million loan from the IMF, the total budget size, the percentage of budgetary reallocation (which is up to 10% per ministry for FY19/20), mechanisms to monitor the plan’s spending have not been confirmed. Even with the reallocation of the state budget, the rationale needs to be transparent. Academics have stated that it makes little sense to cut the budgets of the Ministries of Health, Education, Labor, Immigration and Population and other agencies that are actively fighting COVID-19, and allocating funding from the armed forces and security services would increase the funding for the stimulus package and reduce reliance on foreign debt.

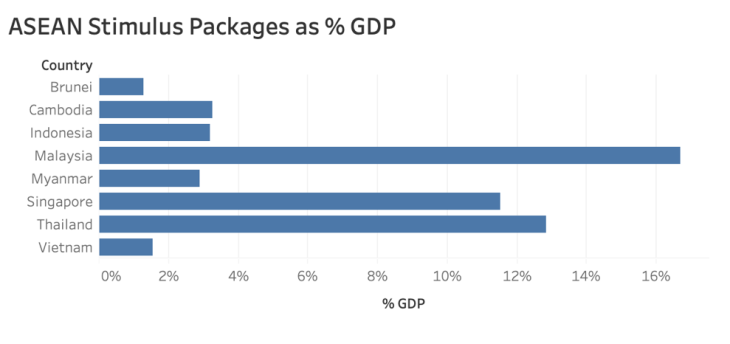

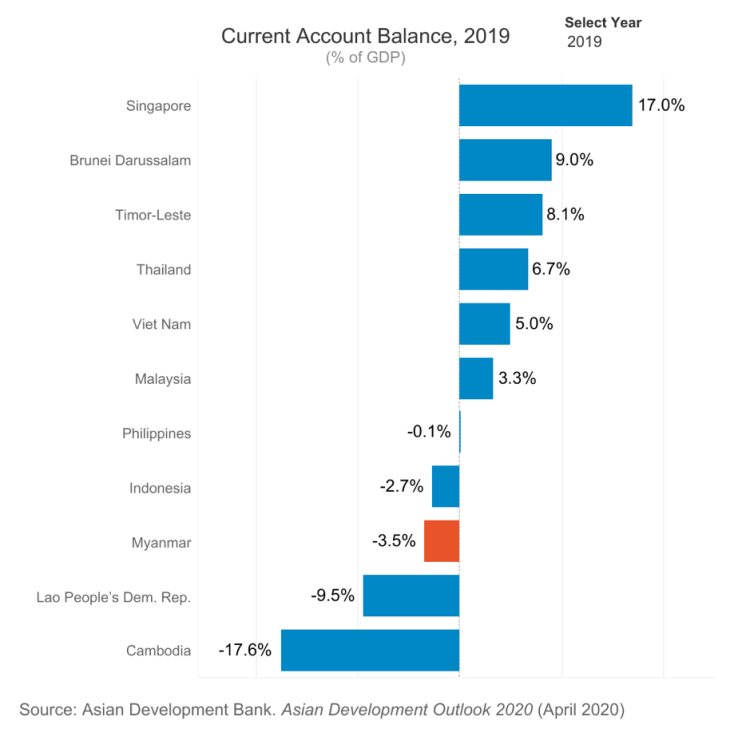

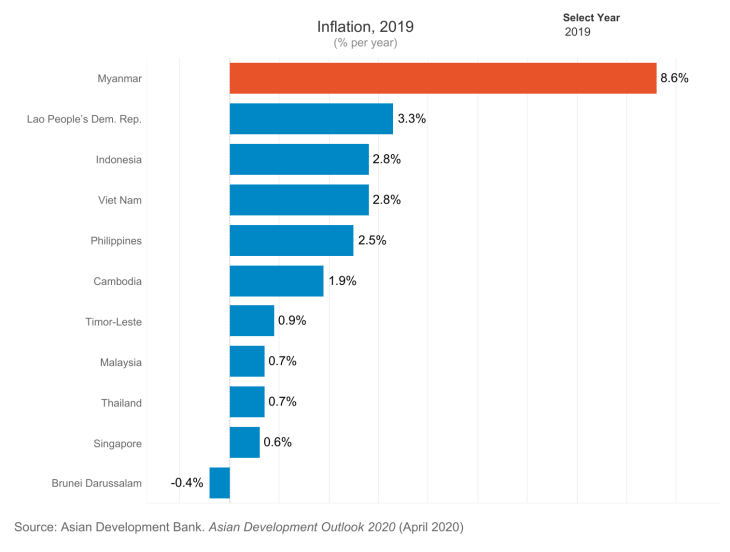

Comparing the Burmese response to its ASEAN neighbors, the CERP is low as a percentage of the Burmese GDP at an estimated 2.91% (Figure 3). It could potentially increase, with the state prepared for a package of up to 5% of its GDP according to Deputy Minister of MOPFI U Maung Maung Win. The stimulus package size is constrained due to current issues of its account balance of -3.5% of its GDP in 2019 (Figure 4) and projected to be -4.5% in 2020, as well as existing levels of private and foreign debt. Countries like Singapore have been able to afford to finance its economic stimulus packages due to the sizable reserves that it has saved for a ‘rainy day.’ Many emerging countries do not have this prerogative and cannot simply print more money, especially with the Burmese inflation rate at 8.6% in 2019 (Figure 5). These factors explain both the modest stimulus package size relative to GDP and the need for international support.

The plan also suffers from implementation issues, missing out key parts of the population due to communication issues. The Burmese government distributed food parcels including rice, salt, cooking oil, lentils, and onions to those without a regular income. The CERP refers to these as “in-kind food transfers to vulnerable households and at-risk populations,” and it is labeled as “done”. The one-time transfer has helped some families, but there are significant pockets of undocumented citizens who have not been eligible, such as slum residents with no address. This is due to the inconsistent communication between the union, subnational, and township authorities, in which the township-level officers had 48 hours to compile a list on who they thought are “vulnerable households” without clear guidelines.

Many informal workers, citizens without documents, populations in conflict areas, rural areas, and rural migrants in cities have fallen through the cracks of this initiative. Without significant changes to these policies, these groups will continue to be excluded from future subsidies. In the meantime, they have turned to microfinance or informal lenders, compounding their existing debt in the hopes that the economy will return. Questions such as “Who is eligible?” and “How long will this last?” must be made clear in the state’s implementation of the CERP. Hence, both the content (i.e. criteria for who is eligible) and mode of communication between the different layers of government need to be streamlined and improved.

Monitoring the progress of the CERP is important to see how the strategies have been implemented and enable pivoting for future strategies. However, the plan’s current monitoring matrix is inadequate in specifying the timeline, cost, and impact. Each goal in the CERP has corresponding action plans, tied to the immediate term’s measurable outputs in a monitoring matrix. Goal 3.1.2. (Easing the impact on Laborers and Workers) states that the “construction of labour-intensive community infrastructures started as much as practically possible before the year-end.” What does “community infrastructure” mean? Where are these, and what constitutes an infrastructural project? How many people are involved? What are the various stages in the infrastructural development that will correspond with these jobs? What happens after the “year-end?” Clear definitions and timeframes are missing from much of the monitoring matrix, and it is indeed difficult to monitor these action plans in its current form. The action plan needs to be presented in phases and a clearer timeline, and answer critical questions about how much each component will cost, and how many people will be included in each phase.

These questions do not preclude ongoing planning and initiatives. The US$18-million Cash-for-Work Program by the Department of Rural Development announced in June 2020 employs villagers to help build basic village infrastructure, expected to benefit about 120,000 households for 3.5 months (mid-June to September). The details for initiatives like this should be included in the monitoring matrix, especially for other programs in various ministries that might already be rolling out. Additionally, ways to identify the action plans’ implementation rate and address any problems during its execution for strategy adaptation would also strengthen the monitoring matrix and program itself.

Furthermore, the plan has to prioritize its strategies to support the vulnerable, utilize consultative channels to enhance the plan’s robustness, and integrate green measures. Without a clear overall narrative logic behind the CERP, several academics such as Walden Bello have called it a “wishful shopping list.” They call for a prioritization of four aspects—immediate public health measures, addressing hunger, mitigating production and employment impacts for smaller businesses with limited cashflow, and recreating more local, community-driven value chains. The clarification of the plan’s priorities would generate better impetus for evaluating the plan’s effectiveness and streamlining the budgeting process.

The lack of consultation about the CERP has also resulted in criticism by key business leaders in the country, as industry-specific measures fall short. There has been some acknowledgement of the plan’s benefits of decreasing bank interest rates, extending the repayment for non-performing loans, and deferring income tax. Nevertheless, these are wholly inadequate, and many businesses continue to struggle. Macro models of the pandemic suggest that sector-specific stimulus may generate the largest stimulus per dollar spent, increasing aggregate demand by choosing non-substitutive industries. This logic cannot be uncritically applied to the Burmese context due to its existing political economic configuration.

To build on this point on sector-specific improvements, business leaders in Myanmar have stepped up to identify several improvements to the plan: agricultural loans should be extended beyond rice farmers; the fishery sector has the potential to bounce back but has been given little attention; tax relief in the CERP makes little sense if there is no economic growth; the 50% guarantee of loans for new investments does not make sense as new investments with the current climate is not likely. These would have been pointed out earlier had they been consulted, which would significantly strengthen the plan.

The inclusion of industry leaders would also enable another point of contact with those sectors. The Asia Foundation’s survey of COVID-19’s impact of businesses between April and May 2020 identified COVID-19’s impact on operations, sales, profitability and cash flow. The results show that nearly two-thirds of businesses have cash flow problems and are at high risk of closing down, and an estimated US$650 million-1.5 billion is needed to support these businesses. Moreover, only 67% of businesses knew about the CERP’s loan program, and only a fraction of government emergency loans had reached them. There are clear and urgent information gaps here. Consulting businesses and a network of industry leaders could enable better information dissemination and allow the state to gain a more in-depth understanding about sector-specific issues and tailor stimulus towards them accordingly.

Lastly, the CERP’s attempts to rebuild Myanmar post-COVID cannot neglect the environment. Myanmar already has the highest air pollution levels in ASEAN and building more coal-fired plants and hydropower dams are not acceptable paths forward. These projects have previously resulted in dispossession, and if continued, will cause thousands of premature deaths per year. Bloomberg Green has put together a menu of 26 green stimulus tools across nine sectors as a resource to build the economy back greener and more sustainably, and the World Bank has a sustainability checklist for economic recovery interventions. Greening the CERP requires both assessing the short- and long-term environmental impacts of the current measures and ensuring strategies are aligned with existing resilient and low-carbon development plans. A post-carbon economy is not a luxury that emerging economies cannot afford and must be better integrated by ‘tilting towards green’ in the ongoing economic recovery from COVID-19.

The state’s cautious approach towards infrastructure projects in the CERP is a positive direction and should continue as well. The CERP’s fast-tracking of many large infrastructural projects to stimulate growth was initially alarming because it might have bypassed social and environmental standards. However, a senior official commented on how several Chinese megaprojects as part of its Belt Road Initiative were not part of the CERP and required proper scrutiny. It would feed into a Project Bank, which is a database of priority projects established with Singapore’s Infrastructure Asia initiative in an agreement with the MOPFI to help identify investors, ensure international standards, tenders, and the projects’ bankability. Due process for these projects’ implementation is important to mitigate environmental degradation though the CERP itself should include greener and more sustainable components.

The economy is reopening but this must be tempered by two developments—the enduring global economic fallout and the possibility of a second wave. This is especially worrying considering that numerous countries are ending lockdowns even as new cases are increasing. No new normal is poised to occur, especially without a vaccine and the projection of deglobalization, higher inflation, and lower growth rates.

This article has laid out the urgent need for the CERP to improve due to the macroeconomic fallout with tangible on-the-ground impacts, and specified three main axes for enhancement—financing, implementation, as well as enhancing social and environmental dimensions. The food transfers, monetary policies, and Cash-For-Work program have been a welcome support but they still exclude many informal workers, businesses, and economic sectors. In its subsequent iteration, the plan needs to clarify its financing with a transparent rationale. The implementation through different layers of government have to be improved both by having clearer messages such as the criteria for who is eligible for transfers, and the mode of inter-scalar communication to ensure accuracy, and that the measures do reach the vulnerable. More robust monitoring mechanisms are required in terms of timeline, impact, and cost. The plan also needs to present a stronger sense of prioritization and be adjusted through consultation for its fiscal stimulus to be optimized with sector-specific strategies. And the CERP’s gaping green hole also needs to be filled.

As former adviser to the President of Myanmar Thant Myint-U states, this is an opportunity for Myanmar to create a “welfare state that provides for all people equally.” There is little room for error and the current rhetoric of the CERP needs to be manifest through kyats in the pockets of those who need it most and ensure a more sustainable, greener new normal.

Al Lim is a researcher of Southeast Asian urban studies. He starts his PhD in Anthropology at Yale University in 2020, after completing an MSc in Urbanisation and Development at the London School of Economics and Political Science and a B.A. (Hons) in Urban Studies at Yale-NUS College. His academic writings have been featured in City & Society, New Naratif, and the Singapore Policy Journal. (Read more on LinkedIn)